Key Takeaways

- Off-plan mortgages help finance under-construction homes, usually after 50% payment and 50% project completion.

- LTV is capped at 50%, so buyers must cover the rest upfront.

- Only select banks offer off-plan loans, mainly for Tier 1 developers like Emaar and Nakheel.

- Funds are disbursed in stages tied to construction milestones, paid directly to developers.

- Choose fixed or variable rates depending on your budget and market outlook.

- Strong ROI potential, but not ideal for buyers who need immediate occupancy.

Let’s break down the “off-plan mortgage in Dubai” so you understand how it works, who qualifies, and what banks are looking for.

What Is an Off-Plan Mortgage in Dubai?

An off-plan mortgage is a home loan granted for a property that is still under development. Unlike traditional mortgages, which are for completed homes, this option allows you to secure a property early—often at a lower price—with structured payments made during construction.

It’s particularly popular among investors seeking capital appreciation and buyers looking to lock in favorable prices.

Why Consider an Off-Plan Property Mortgage in Dubai?

There are several reasons why investors flock to off-plan properties:

- Lower entry costs: Off-plan units are often priced lower than completed properties at the time of purchase, offering early buyers the advantage of pre-completion rates.

- Flexible payment plans: Developers often accept payments in stages.

- High ROI potential: Property values often rise significantly by completion.

- Customization: Some developers let you tailor interiors and layouts.

But to make this work, you need to understand the financing structure.

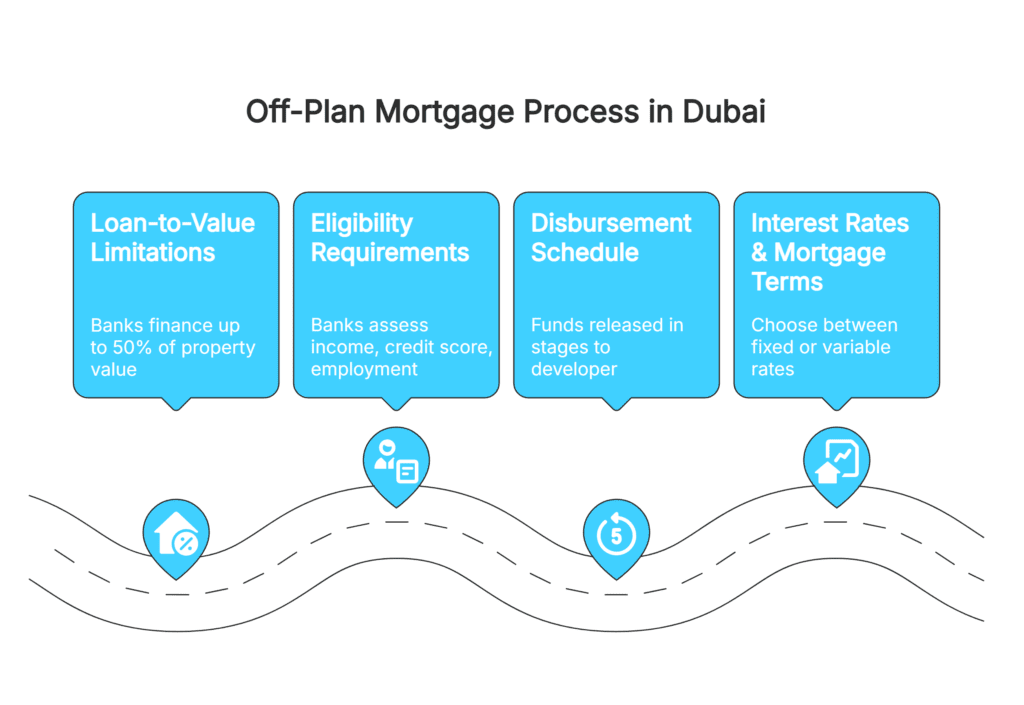

How Does an Off-Plan Mortgage Work in Dubai?

1. Loan-to-Value (LTV) Limitations

Banks only finance up to 50% of the property value for off-plan units. This means you’ll need to pay the other 50% out-of-pocket.

Example: If the unit costs AED 2 million, banks will lend up to AED 1 million.

Tip: You must already have paid 50% of the property cost and 50% of construction must be completed before mortgage funds are released.

2. Eligibility Requirements

Banks will assess:

- Your monthly income

- Credit score

- Employment status

- Age (must complete loan by retirement age—65 for employees, 70 for self-employed)

Foreign buyers are eligible, but down payment requirements are stricter—especially for non-residents.

3. Disbursement Schedule

Funds are released in stages, matching construction milestones. The money goes directly to the developer, not the buyer. This ensures banks only pay for work that has been completed and inspected.

4. Interest Rates & Mortgage Terms

You’ll typically choose between:

- Fixed-rate mortgages: Predictable payments over 5–25 years.

- Variable-rate mortgages: Rates that fluctuate with the market (based on EIBOR).

Rates vary from bank to bank. Comparing offers is critical.

Which Banks Offer Off-Plan Mortgages in Dubai?

Not all lenders support off-plan financing. Banks usually approve projects developed by Tier 1 developers such as: Emaar, DAMAC, Nakheel, Dubai Properties, Meraas. Each bank also maintains an internal list of “approved projects.” Mortgage approval will depend heavily on the developer and project’s progress.

Fixed vs Variable Rate Mortgages for Off-Plan

When financing an off-plan property in Dubai, choosing between a fixed or variable interest rate can impact your long-term financial strategy. Here’s a breakdown of both options:

Fixed Rate Pros:

With a fixed-rate mortgage, your monthly payments stay consistent throughout the loan term. This predictability makes budgeting easier and provides peace of mind, especially for first-time investors or end-users looking for financial stability.

Fixed Rate Cons:

The main drawback is that fixed rates usually start higher than variable ones. If the market interest rates drop, you won’t benefit from the savings. Plus, breaking out of a fixed-term early can sometimes involve penalties.

Variable Rate Pros:

Variable-rate mortgages often begin with lower interest rates, which can mean lower initial payments. If Dubai’s lending rates decrease over time, you could end up saving significantly compared to a fixed-rate option.

Variable Rate Cons:

The downside? Your payments may rise unexpectedly if the market shifts. This unpredictability can make budgeting harder and may not suit buyers who prefer financial certainty in a fluctuating market.

| Characteristic |

Fixed Rate |

Variable Rate |

| Predictability |

Predictable payments |

Payment fluctuations |

| Initial Rate |

Usually higher |

Lower starting rate |

| Flexibility |

Less flexibility |

Potential cost savings |

| Market volatility |

Easier planning |

Unpredictable payments |

Choose what suits your risk tolerance and budget strategy.

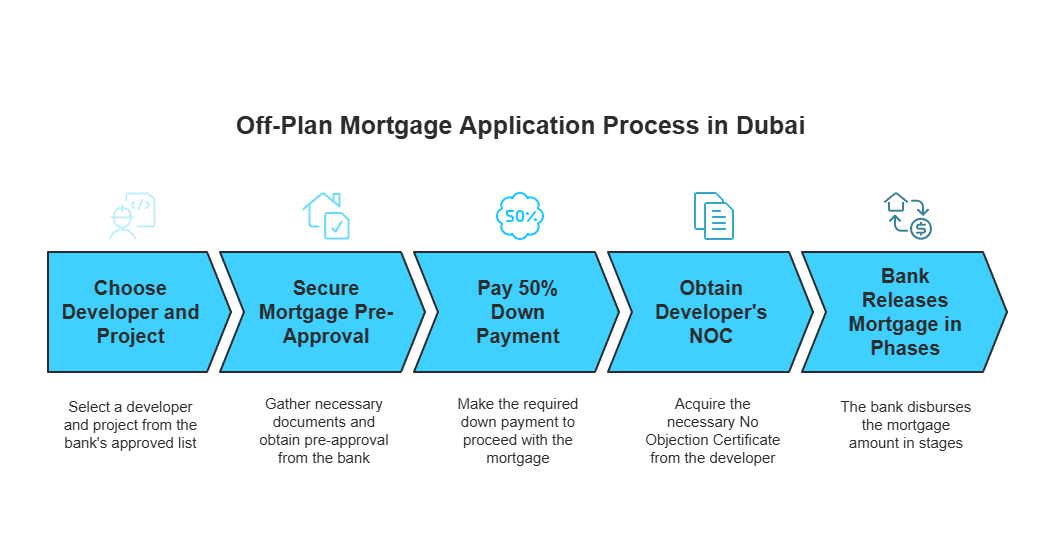

Step-by-Step: How to Apply for an Off-Plan Mortgage in Dubai

- Choose a developer and project: Ensure the developer is on your chosen bank’s approved list.

- Secure mortgage pre-approval: Typically takes 3–5 working days. You’ll need:

- Emirates ID

- Salary certificate or company license (for self-employed)

- Recent bank statements

- Down payment proof

- Pay the required 50%: No bank will finance until this is paid upfront by you.

- Get the developer’s NOC: Required to proceed with the bank mortgage disbursement.

Bank releases the mortgage in phases: Each phase matches the construction progress.

Can You Sell an Off-Plan Property with a Mortgage?

Yes, off-plan properties under mortgage can be resold (via property assignment). You’ll need to:

- Get NOC from the developer

- Pay any early settlement fees to the bank

- Coordinate with the buyer’s bank if they also require a mortgage

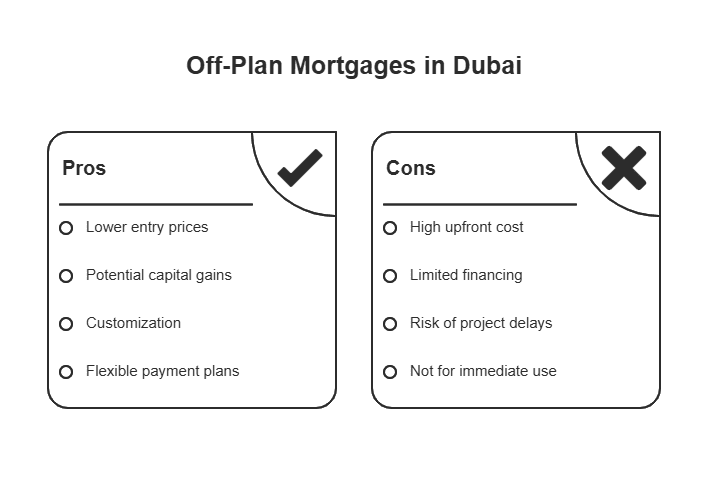

Pros and Cons of Off-Plan Mortgages in Dubai

Off-plan mortgages in Dubai come with both unique benefits and certain limitations that buyers should consider before committing.

One of the main advantages is the lower entry price compared to completed properties. Buyers also stand to benefit from potential capital gains by the time the property is handed over, especially in growing areas.

Another plus is the ability to customize layouts and finishes during the construction phase, which is often not possible with ready properties. On top of that, developers typically offer flexible payment plans spread out over the construction period.

However, most banks require buyers to pay at least 50% of the property price before releasing mortgage funds. Additionally, only a limited number of banks in the UAE offer financing for off-plan purchases. Delays in construction can also impact your move-in timeline. Finally, off-plan properties aren’t ideal for those who need immediate housing, since handover can take several years depending on the development.

Conclusion

Off-plan mortgages in Dubai are a solid financing option—if you plan ahead and know what you’re doing. The low price points and growth potential make these deals very attractive, especially when working with major developers like Emaar or DAMAC.

But, they come with strict conditions—especially the 50% upfront payment and limited LTV. With smart planning, the right bank, and professional mortgage services in Dubai, you can unlock a strong investment opportunity in one of the world’s most dynamic real estate markets.

FAQs

Can expats get an off-plan mortgage in Dubai?

Yes, but expats may need to pay a higher down payment (often 50%) and show strong income proof.

Is the interest rate higher on off-plan mortgages?

Not necessarily. Rates vary based on fixed vs variable choices and your financial profile.

Can I get a mortgage for a property that’s only 20% complete?

No. Most banks require at least 50% construction and 50% payment made before disbursement.

How long is the mortgage term for off-plan homes?

Typically 5–25 years, but some banks offer up to 30 years depending on the borrower’s age and financial profile.

Do all banks offer off-plan financing?

No. Only selected banks offer mortgages for off-plan units—and mostly for Tier 1 developers.